The recommendations on the actuarial interest rate in personal injury cases: an attempt to unify the actuarial interest rate discussion

October 2021

In the Netherlands, the actuarial interest rate in personal injury cases has always been a subject of discussion. In view of the discussion, two groups of experts have developed Recommendations on the Actuarial Interest Rate in Personal Injury Cases (hereinafter: the "Recommendations"). The Recommendations are intended to increase legal equality, legal certainty and efficiency in the debate between insurers and victims.

In this blog, we will briefly discuss the concept of the actuarial interest rate, after which we will discuss the new Recommendations. Finally, we will make a comparison with the system in the United Kingdom.

What is the actuarial interest rate?

In order to be able to settle all personal injury claims of a victim at once on a certain reference date, insurers and victims estimate the future damage of the victim. The future damage includes damage items such as loss of ability to work, loss of self-sufficiency and compensation for pain and suffering. In practice, they often look at what the damage will be per future year. The total amount of these annual damages must then be capitalized. For this purpose, the actuarial interest rate is used.

To determine the percentage of the actuarial interest rate, the expected return on the amount to be paid out at once is taken into account, as well as the expected inflation. The inflation is then deducted from the return as the actuarial interest rate. This is a kind of "reverse calculation": based on the total amount of the annual claims, it is determined which amount must be paid out on the reference date, so that the victim can actually bear his future loss.

So far, insurers have often used an actuarial interest rate of 3% (a 6% return minus 3% inflation). This percentage was the subject of increasing discussion. Reality showed that a 6% return was hardly ever achieved and that an inflation rate of 3% was not in line with reality. The actuarial interest rate, therefore,

For this reason, an attempt was made to reach agreement on the actuarial interest rate to be used in the form of the Recommendations issued by the National Consultative Committee on Civil Procedure and Cantonal Proceedings (the LOVCK) and the National Consultative Committee on Civil Procedure in the Courts (the LOVCH) in June 2021.The LOVCK and the LOVCH are two consultative or advisory bodies that make recommendations to the judiciary in all kinds of legal and other fields in order to promote uniformity in the administration of justice.

Recommendations

On 13 May 2020, the District Court of The Hague rendered a judgment that can be regarded as the predecessor of the Recommendations. We also refer to the previous blog of Arian Lengton and Ronna Rutten. The National Expert Group on Personal Injury, which advises the LOCVK and the LOVCH, had made proposals for the Recommendations, partly as a result of this court ruling.

It is important that the Recommendations explicitly state that they are recommendations. Judges are free to depart from them if there are good arguments for doing so. Moreover, the judges are of course bound by the party debate.

Furthermore, the starting point is that the victim must actually be able to bear his future loss. According to the explanatory notes to the Recommendations, the interests in setting the actuarial interest rate are great. An excessively high actuarial interest rate may result in a victim who annually withdraws and uses the budgeted annual damage, having already exhausted the compensation a number of years before the calculated end date. Moreover, it is not desirable for a victim to take risks when investing the lump sum received in order to ensure payment of his annual damage until the final age.

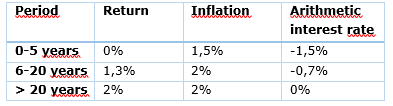

In concrete terms, the Recommendations are based on three periods. Each period has its own percentage based on its own assumptions. The return and inflation assumed by the Recommendations for each period is as follows:

With regard to the return, the Recommendations are based on, respectively, the average interest rate on an ordinary savings account, the average interest rate on a savings deposit for 5, 10 and 15 years, and the interest rate component of the UFR. With regard to inflation, the Recommendations are based on the forecasts of the Dutch Office for Economic Policy Analysis and the rate which the European Central Bank is aiming for and which is also roughly in line with the long-term average inflation rate.

In general, the Recommendations have been well received by the Dutch Association of Insurers, although in practice this will mean that insurers will have to pay out a higher amount due to the currently negative or neutral actuarial interest rates. The Recommendations are also well received by victims because they create clarity. Of course, there are still points for improvement. Criticism is mainly voiced for the calculation of the return and inflation. Partly for that reason, the Recommendations state that they will be reviewed once a year and, if necessary, adjusted.

The Recommendations have been used by the Court of North Netherlands. The Court recently ruled that the actuarial interest rate that follows from the Recommendations contains a realistic estimate of the return that the victim in question will be able to achieve on his damages and of the inflation that will occur in the course of time.[1]

Comparable to the discount rate in the United Kingdom

In the United Kingdom, a uniform system for the actuarial interest rate has been in place for some time. Various authors have argued that this approach should also be adopted in the Netherlands, because the UK approach is based on reality rather than fictions and abstractions.[2] It appears that this view has now been heard.

The UK system uses the discount rate to determine the capital to be paid for future personal injury and death.[3] This is comparable to our actuarial interest rate. A working group of actuaries, accountants, lawyers and insurers determine this discount rate under the direction of the government. They take into account the developments on the financial markets during the past years and the expectations for the future.[4]This working group publishes its findings in the form of guidelines, the "Ogden tables". In 2020, the eighth edition of the Ogden tables was published.

In the United Kingdom, the discount rate has been lowered in recent years. Currently, a discount rate of -0.25% is assumed. This also takes account of the fact that claimants are seen as risk-averse investors.[5]

Conclusion

Although there are some critical voices from practitioners about the Recommendations, particularly with respect to the way in which the expected rate of return and the expected inflation are determined, most voices are positive. The aim is to reduce the discussion about the actuarial interest rate in personal injury cases. By using fixed percentages the victim, but also the insurer, knows where he or she stands. The future will show whether judges will actually use the Recommendations and whether the percentage is sufficient.

* * *

[1] Court of North Netherlands 31 August 2021, www.letselschademagazine.nl/2021/RBNNE-310821.

[2] See, for example, J. Keizer, ‘Schadevergoeding via een som ineens, rekenrente en financieel advies. Waarborgen dat het slachtoffer zijn toekomstschade daadwerkelijk kan dragen’, Letsel & Schade 2018, nr. 3, p. 12.

[3] J. Keizer, ‘Schadevergoeding via een som ineens, rekenrente en financieel advies. Waarborgen dat het slachtoffer zijn toekomstschade daadwerkelijk kan dragen’, Letsel & Schade 2018, nr. 3, p. 11.

[4] R.M.J.T. van Dort & E.S. Groot, ‘De redelijke verwachting ten aanzien van de rekenrente’, TVP 2019, nr. 3, p.91.

[5] R.M.J.T. van Dort & E.S. Groot, ‘De redelijke verwachting ten aanzien van de rekenrente’, TVP 2019, nr. 3, p.91.