Negative actuarial interest, something to take into account when calculating a personal injury loss

June 2021

Introduction

About a year ago, the District Court of The Hague ruled a very interesting verdict[1] regarding the effects of actuarial interest on future losses in case of personal injury. The Court ruled that for the short and medium term, it is considered reasonable to apply a negative actuarial interest. This may well lead to higher losses, although as yet, the effects in practice appear to be remote. But what is ahead of us?

Substance

In case of a personal injury claim, usually the victim is granted a lump sum that covers both the damage that has already been suffered, as well as future damage. For many reasons, this is considered favourable over the alternative, which would be providing advance payments regularly and, at the end of each year, make up the final overview for that year and close any possible gaps.

When providing a sum of money that covers future damage as well, this future damage needs to be capitalised. This means that both interest and inflation need to be offset (as are tax components). Starting point in case of personal injury, is that the victim is fully compensated for the loss that was caused to him by a third (liable) party. This means that when calculating the amount of future losses, no or at least no more than negligible risks can be expected from the victim in his financial planning and allocation. The victim needs to have much security that he will be able to release his yearly damage from the total amount that was provided to him.

Historically in The Netherlands, the so-called 6 – 3 norm was applied. In general, one was expected to be able to make a return on investments of 6%. Inflation was set a 3% which led to an actuarial interest of (6-3=) 3%. Based on this actuarial interest, parties calculated the compensation that was needed to indemnify the victim for its loss. However, the times of 6% interest and 3% inflation are well behind us. What bank is willing (and able?) to compensate interest of 6% over the last years? And also, inflation was not up to 3% but significantly lower than that. This did not go unattended by the parties who are involved in personal injury claims. Attempts were undertaken by representatives of all stakeholders to come up to a new, more up to date norm (than the 6-3), but this was unsuccessful. Eventually, the District Court of The Hague stepped in and provided guidance. As the District Court of The Hague has a specific and reputable personal injury department, we consider it likely that this verdict will play a decisive role in future personal injury settlements.

The verdict

The facts of the claim itself are not very rare or leading to the result. Although a personal injury is always sad for the parties involved, this claim is like many others. Liability was accepted, but there was (much) discussion regarding mainly future loss of income. We will leave the facts as they are and will directly deal with the Court’s considerations.

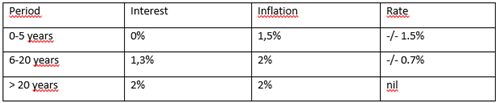

The Court starts with the rather general principle that future development of interest and inflation are best approached by the Court’s reasonable expectations. The Court confirms that the victim effectively needs to be able to bear his future losses from the agreed settlement amount. If the adapted interest rate is too high or the inflation rate is too low, this could well lead to the situation where the agreed lump sum is insufficient to cover the entire period that was agreed upon when making the calculations for the settlement amount, only because the actuarial interest rate did not match reality. According to fixed case law, the liable party cannot expect the victim to take serious risks and invest its money in funds that could lead to losing parts of this. Only solid investments are allowed to be taken into consideration when calculating possible ‘growth’ of the granted amount of money. As risk and reward tend to go hand in hand, these solid investments will generally pay out much less return than other, more risky investments. In defining a realistic approach on both interest and inflation, the Court has come up with 3 time periods which are short term (0-5 years), middle term (6-20 years) and long term (> 20 years), each category with its own interest and inflation percentages.

Short term (0 – 5 years)

In respect of the first five years after capitalization, the Court rules that it is hardly impossible to invest money for this short period of time as it is likely that the victim will need this money within this period. To determine the interest rate, the Court looked at the rates banks are offering for regular saving accounts. As this rate is nil at the moment, so is the percentage that needs to be used for calculation purposes. Regarding the inflation rate, the Court embraces the expectations of the Netherlands Bureau for Economic Policy Analysis (CPB) over this period of time, which is 1,5%.

Mid-term (6 – 20 years)

Regarding the mid-term, the Court rules that it is reasonable that the victim will invest the money in low risk investments, such as deposits. Because the victim should be able to withdraw sums of money from the investment (in order to bear the costs of living) the Court divides this period of 15 years over 3 periods of 5 five years. The Court determined the rates for these three periods based on the offers of Dutch deposit providers over 5, 10 and 15 years. Accordingly, the Court set the interest rate at 1,3%.

The Court based the inflation rate on the long term goal of the European Central Bank, which is 2%. The Ultimate Forward Rate (UFR) also takes into account a 2% inflation rate.

Long term (> 20 years)

In respect of the long term, the Court applies the UFR rate that is used by the Dutch pension funds. This UFR is calculated, based on the 120 months average and shows the market expectations of what will be the interest rate over the upcoming period. At the time of the verdict of the Court (May 2020), this UFR was 2%.

The inflation rate for the long term has also been set at 2%. All-in all, this leads to the following rates:

The consequences

For the short and middle term, the Court is adapting a negative interest. This is unprecedented. To compensate the damages, not only the actual loss needs to be paid, but this amount needs to be added with a surplus to cover the difference between return and inflation.

By means of calculation exercise: if the yearly damage is EUR 100, the liable party does not need to pay EUR 100 over the first year, but EUR 100 + compensation for 1.5% negative interest (so therefore EUR 101.50). And over the second year, 1.015% over EUR 101.50 (= EUR 103.02). And so on. From year 6, the rate changes from -/- 1.5% to -/- 0.7, but this is still negative. A surplus therefore still needs to be added to the loss itself, in order to take away the depreciation. There is not much explanation needed to determine this will lead to an increased burden of claims.

Conclusion

The question is if and in what way this verdict will have an impact on future settlement negotiations. Will insurers adapt their claims (and reservation) policy? And will personal injury lawyers adapt their strategy? Time will tell. Based on our conversations with insurers, the verdict has not yet affected the burden of claims substantially. At the same time, personal injury claims do take a long time to get to an agreement. A rise in burden of claims may therefore well be under the surface. We will keep a close watch on the developments and inform you if and when appropriate.

* * *

[1] District Court of The Hague, May 13, 2020, ECLI:NL:RBDHA:2020:4169.